Looking into 2024 for Multifamily in Florida

Insurance, interest rates, supply and demand

It’s 2024 and it’s been several weeks so here are a few updates or annotations on what we’re seeing and experiencing. This will probably be a shorter post than others, but but you might appreciate that as you ease back into work mode after the holidays.

Insurance

The main bane of FL property owners for the past 2-3 years and oh what a ride it’s been. It continues to trend upward, but maybe some respite ahead? For the very first time in a long time, I had my first conversation with our main insurance broker that there might be light at the end of the tunnel. Losses have apparently stabilized and there might be increased interest in carriers to re-enter the market which would create more competition and hopefully stabilize or reduce premiums. We both somewhat agreed if anything like this does happen it’s still a way off, maybe later this year, maybe 2025, or maybe even longer. I don’t think it’s anything too quick and will feel more like trying to turn a large oil tanker rather than a jet ski.

But it’s the first hint at even some good news on the insurance front, so we’re grasping at that straw and clutching it tight.

Interest Rates

Maybe you’ve heard the FED change its tune in December about rate hikes turning to a rate pause and maybe some cuts in 2024.

The Fed said in its policy statement that it will maintain the federal funds rate in a range of 5.25% to 5.5%, marking the third consecutive pause since July, when it last raised rates. Federal Bank officials also signaled the benchmark rate could be cut by 0.75% percentage point in 2024, according to a chart that documents their projections.

So we had the 10-year treasury go from 5% to 4% very quickly and this has helped a lot of people with their loans in the short term.

Sounds like good news right?

Well, maybe not.

Some are saying that the FED changing its tune means they see a problem looming and are going to reverse course to try and prevent it. So maybe interest rates go down, but unemployment goes higher and property owners experience higher vacancy, bad debt, turnover, etc.

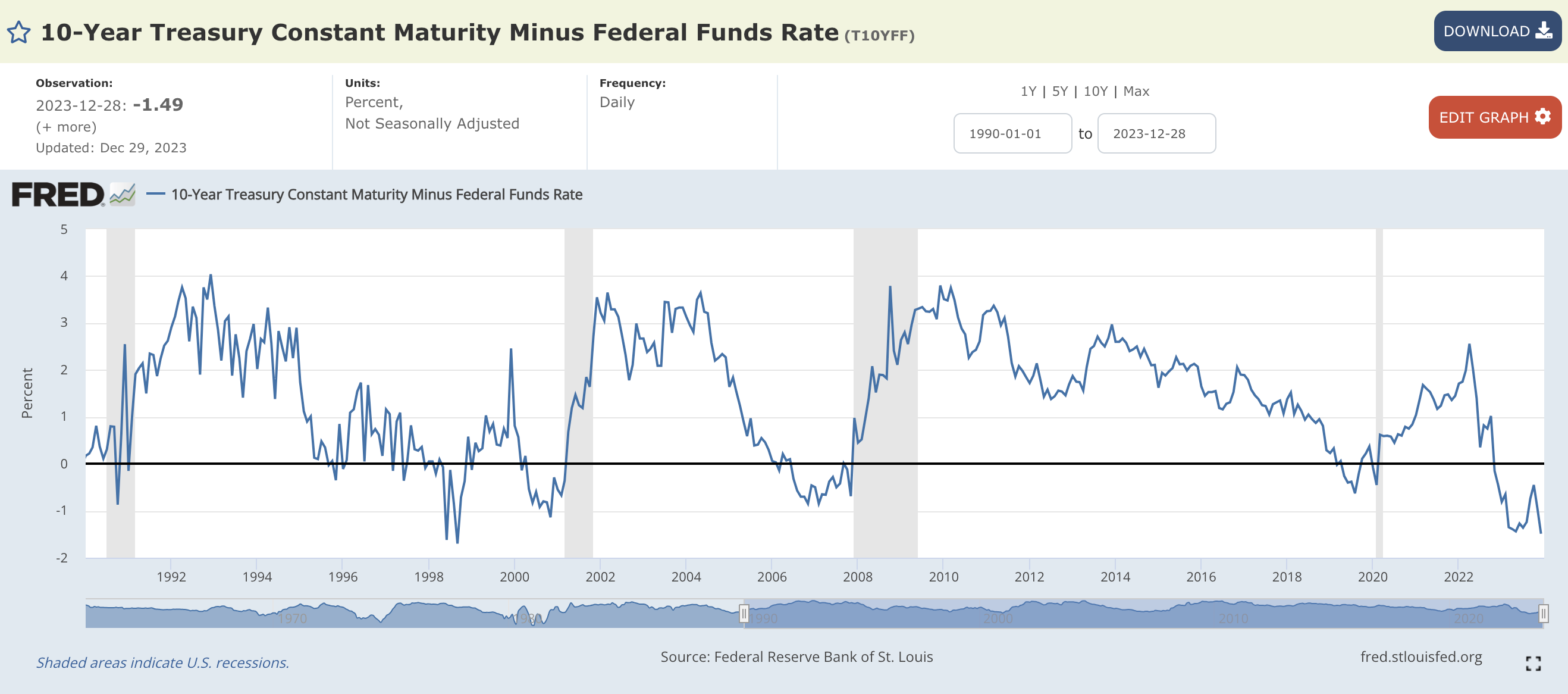

Another factor to consider is right now we have an inverted yield curve and have had that for some time. Historically this is not normal and is a sign of a recession. So even if we have the federal funds rate get cut from 5% to say 4% or even 3.5%, what happens if the yield curve reverts back to its usual positive slope?

Take a look at this graph comparing the difference of the 10-year treasury minus the FED Funds rate. Usually, it is positive going back to 1990, and we see a fairly healthy amount over it. So, in theory, if we had a federal funds rate go down to 4% but the yield curve reverts, that could mean the 10-year goes up above 4%. The graph has a spread of anywhere from 0-4%.

Your guess would be as good as mine.

But here is a slightly different version showing what each yield was going back to 1990, but is slightly out of date being taken from July 2023.

So if it reverts but the federal funds rate is in the 3-5% range, does that mean treasuries will be 100 basis points higher? 150? Flat?

I certainly don’t know, but the fact that the federal funds rate may or may not get cut this year, doesn’t necessarily mean the 10-year treasury will also come down. And then you have to factor in what spreads for lenders are also going to be and if they’re shrinking or expanding.

The bottom line is nobody knows, and anyone who tells you your mortgage rates will definitely be lower this year has something to sell you.

Supply and Demand

There’s a common thread being pulled here, and if you can spot the supply and demand in the last two categories, congratulations. But this one is going to be spelled out in black and white.

We still have extremely high levels of new housing units being completed in Florida. Development is a 3-7 year process depending on the project, so deals being completed this year are too far along to stop now unless we have an X-level event that halts these projects in their tracks. But nothing is so bad right now that this is happening across the board, so most projects are finishing up and making the most of it.

So for this year, and maybe even next year too, Florida is still fighting against lower rent growth and continually increasing expenses. This is not a good recipe for owners or prospective buyers. So buyers are pricing in these challenges, but owners aren’t forced to sell yet at lower valuations except in the worst of situations.

So Supply continues to get churned out, and it’s fairly level with demand from renters or slightly more than demand. Which leads us to flat or slightly declining rents on average.

However, these market forces have slowed down new construction starts, so there is probably light at the end of the tunnel sometime later in 2024, 2025, or maybe in 2026. As long as demand doesn’t start to dry up (larger unemployment, slower population growth, etc.) then supply should eventually ebb back down and owners should see some better rent growth and occupancy in the future.

What are we doing?

We are still looking at deals, but listings are still way down, and for deals we are seeing we are pretty far off the asking amounts. So we are sitting tight and being patient until we find deals that make sense given the market conditions we are currently in. So until pricing changes or market conditions change, we will continue to be patient.

Here’s to a great 2024!

Chris Grenzig

Chris@jag-communities.com

jagcapitalpartners.com